wind POWER

Setting a course for 33 GW of offshore wind in the UK

1 September 2009The UK government has put in place a raft of measures supportive of offshore wind. But challenges remain.

Offshore wind development is fundamental to the UK government’s renewable energy aspirations, and a number of recent initiatives aim to accelerate the process.

As its contribution to the EU’s 2020 target, the UK has a legally binding commitment to obtain 15% of its energy from renewable sources by 2020. Recent UK government modelling suggests that renewables could provide at least 30% of the country’s electricity by that date (compared with 5.5% now), with wind providing about two-thirds. In turn offshore wind could exceed the contribution from onshore sites and become the largest single energy source among the renewables, accounting for about a quarter of total electricity supply.

Under the just completed Strategic Environmental Assessment (SEA) it has been concluded that 25 GWe of additional offshore wind should be permissible without “unacceptable environmental impacts at a strategic level” in English and Welsh territorial waters and the UK Renewable Energy Zone, up to 60m depth by 2020. This would be in addition to the 8 GWe of offshore wind currently in operation, under construction or firmly planned.

Completion of the SEA enables the Crown Estate (the leasing authority for offshore wind developments) to proceed with its Round 3 leasing competition, leading to the award of development rights to the winning bidders. The plan is to enter into Zone Development Agreements with the preferred bidders by the end of the year. The Crown Estate said it had received “multiple bids for each of the nine zones” by its deadline of 3 March.

In Round 3 the Crown Estate is planning a more prominent role, including co-investment with developers. The Crown Estate has already committed to direct investments in wind technology, notably in Clipper Windpower’s Britannia project, which is aiming at developing a 10 MW offshore wind turbine. It has agreed to purchase the prototype Britannia turbine to allow it to “gain first hand knowledge of the challenges facing the development of wind turbines specialised for deep water marine deployment as the process of engaging industry to develop the next phase of offshore wind farms begins.” Britannia design completion is scheduled for the end of 2009 and component testing is planned to start in 2010.

The government says it “has earmarked up to £120 million to support a step-change in investment in the offshore wind industry in the UK. This includes funding for new offshore wind energy manufacturing facilities in the UK; investment in the development of next-generation and near-market offshore wind technologies through large scale demonstration; and improving the UK’s capability in integrated offshore wind testing, including through dedicated testing facilities.”

Recent specific measures supportive of offshore wind include the following:

• Proposed increased financial support (potentially amounting to £2-3 billion) for offshore wind, with ROCS (Renewables Obligation Certificates) going to 2 per MWh. The level was recently raised to 1.5 under the new “banded” RO scheme. The additional increase, proposed in this year’s annual government Budget, reflects recognition that the costs of offshore wind farms reaching financial close have risen markedly in the past few months.

• “Go-Active” of a new offshore grid regime. This involves competitive tendering by Ofgem to appoint new offshore grid companies – “OFTOs” (Offshore Transmission Owners) – to build and operate the offshore grid needed for offshore wind expansion. Basically, under the new scheme generators will set out their transmission needs and Ofgem will then market the tender, evaluate the bids and grant the OFTO licence to the successful bidder. The exercise is said to have “the potential to save generators £1bn by getting the best deal.” The first tender round, covering £1 billion worth of existing transmission assets, has been launched, with the first OFTO licences to be issued by June 2010, when the new regime becomes fully operational and it becomes prohibited to transmit electricity offshore at 132 kV and above without a licence. For these projects already built (or being built) bids are being invited to own and maintain the existing assets. Ofgem will place a value on these assets that the OFTO will pay to the generator.

The competitive tender process, designed to attract “new entrants with transmission expertise”, is, according to Alistair Buchanan, Chief Executive of Ofgem, a “huge opportunity for investment under a long-term, low-risk regulatory regime.” The government and Ofgem are working with the European Investment Bank to secure funding to support delivery of the new network. The co-ordinating role of National Grid (onshore HV system owner and operator) has been extended to offshore and it will be responsible for overseeing connections to ensure that all generators that want to connect to the onshore grid can. National Grid is developing (with inputs from the Crown Estate) an “Offshore Development Information Statement” to be completed by the end of the year, reflecting current industry views on the potential shape of future offshore networks.

• Streamlining of the planning process for “nationally significant infrastructure projects”, including offshore wind farms over 100 MW, with the aim of providing planning decisions within 9 months of the start of the examination process. As from 2010, such decisions will be taken by a new body, the Infrastructure Planning Commission (although the Conservatives have said they will scrap this should they win the next election). In addition the government is aiming to rationalise and simplify regulation of the marine environment through the Marine Bill, currently going through parliament.

• Publication of the Renewable Energy Strategy, which sets out a package of measures for meeting the UK’s share of the EU 2020 target.

• Setting up of the new Office of Renewable Energy Deployment.

• Publication of a policy document, A prevailing wind: advancing UK offshore wind deployment, setting out the work that government plans or has already begun, to enable massive expansion of offshore wind.

• The government has declared its intention to “go on supporting the UK supply chain to enter the wind market, seeking out new companies ripe for diversification from the aerospace, defence or automotive sectors.” And following on from the ports report published earlier this year, says it will “do more to support the development of key infrastructure needed for renewable manufacturing operations.”

• Bids have been invited for a £10 million fund to demonstrate next generation offshore wind technology, and the Energy Technologies Institute and Carbon Trust are also providing support for demonstration activities.

Mind the gap

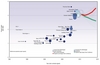

The UK has accounted for an increasing share of global offshore wind new-build in recent years (Figure 1) – currently having more offshore wind installed capacity than any other country (although it remains a small fraction of onshore capacity (Figure 2). And the offshore wind industry has generally welcomed the UK government’s creation of a supportive environment for further growth.

Nevertheless a recent report commissioned by BWEA from Garrad Hassan (now merged with GL) has identified the potential for a hiatus to develop in UK installation activity in a few years time.

The report, UK offshore wind: staying on track, is largely based on interviews with developers, supplemented with published data. It looks at the installation programme for UK offshore wind until 2015, predominantly capturing the delivery of Crown Estate Round 2 projects.

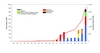

This shows installation, by 2015, of 5.5 GW of total capacity. The build rate of offshore wind since 2007 has slightly exceeded previous BWEA forecasts (2007) and the forecast out to 2012 sees no significant change from the 2007 estimate.

But unless action is taken to influence plans, the analysis shows a ‘gap’ developing in installation activity in the period 2013 to 2015 as the bulk of Round 2 developments are completed but before all but the most advanced Scottish Territorial Waters (STW) projects approach construction (Figure 3).

“This gap is unhealthy for the maturing market and risks losing momentum and therefore supply chain investment,” says the report.

“Although offshore wind will be a much more substantial market in the next five years than it was in the past five years, the absolute level of annual installation will remain inadequate to bring the industry to maturity (in terms of contractor competition) and provides limited potential for inward investment in UK facilities,” it concludes.

What is to be done? The report says sustained growth out to at least 2015 is crucial. One option would be to rely on other EU offshore wind markets (most obviously Germany and Denmark) to provide continuity of demand through the lull. Another is to address the factors which are reducing project capacity (by 1 GW in the case of Round 2) and slowing the Round 2 installation programme (with 1.5 GW of Round 2 projects still to be built after 2015). A third option mentioned in the report is to pursue extensions to Round 1 and 2 projects. In a 29 July announcement the Crown Estate said it was doing exactly this.

Capital cost scenarios

Another recent report, also commissioned by BWEA from Garrad Hassan, aims to assesses how the capital costs of UK offshore wind might develop over the next five years.

The report, UK offshore wind: charting the right course, carried out in consultation with project developers, key supply chain contractors and financiers notes that, although UK offshore wind build in 2009 is expected to be similar to onshore wind build for the first time, this progress has been accompanied by a sharp increase in capital costs, which is “a concern for continuation of that success story, with economic viability now a major barrier to deployment for offshore wind projects.”

The report presents an overall picture of capital costs of offshore wind projects, historically and under current market conditions, Figure 4.

Figure 4 also shows future projections, described as “high and low offshore wind supply chain confidence scenarios.” Supply chain confidence is seen as a key factor in future costs, the report says, and one which can be influenced by policy-makers and developers. In an otherwise neutral environment, projections show that good progress on this front will see capital costs reduced by 15 -20% in five years’ time and on a “strongly-reducing trajectory.”

Other drivers of capital costs tend to be the prosperity of the global onshore wind business and the macro-economic situation, and so less amenable to influence.

A review of the historical offshore wind capital costs reveals several important influences that have driven an upward spiralling trend from around 2005, which followed a period of relative stability from 2000 to 2004. Most important amongst these are those factors that have served to reduce supply chain competition, namely, the ongoing withdrawal of key contractors and products (presumably one product the authors have in mind here is the 4.5 MW offshore machine that Vestas suspended work on a few tears ago) in combination with increasing demand pressure from industries competing for common supply capacity, in particular onshore wind. To reverse the upward capital cost trend in the long-term, a reversal in supply chain trends is important. Another factor that has had a strong historical influence is the relatively high early competition between suppliers (2000-2004) and subsequent losses as the true cost base and challenge of the technology was established and priced into future contracts.

More recently, currency and commodity markets have played an important role. Over 80% of UK offshore wind project capital value is imported, so the devaluation of sterling since 2007 has forced prices sharply up.

Consultation with developers and contractors suggests current capital costs lie in a range centred on £3.1 million per MW installed (for those projects recently contracted and likely to be contracted shortly).

The consensus on future trends is for a slight rise in the next two years followed by a slight fall from current levels to 2015.

The report says there was wide acknowledgement that capital cost reduction was needed for a healthy long-term industry but “attitudes towards the UK offshore wind sector are positive – in some cases very positive indeed” and the 2009 Budget proposals referred to above have been mostly well-received.

The current global offshore wind installation rate is just under 1 GW per annum, over half in the UK, and growing fast. Discussions with wind turbine suppliers identified that they view offshore sales of around 1 GW per annum as the level which would make them consider the offshore business to be close to mature. At this level on a national basis, suppliers may also start to justify inward investment. As there are three to four turbine suppliers active in the market, that would “suggest annual deployment rate of circa 5 GW being required across European offshore markets for maturity in the turbine supply element.”

The offshore wind supply chain is maturing slowly and the extent to which confidence building can be accelerated has a substantial impact on overall capital costs over a five-year horizon, or more importantly, the trajectory which capital costs will be following by 2015, the report’s authors believe. “If sufficient confidence is instilled for incumbent and new-entrant suppliers and contractors, a dedicated supply chain could be created for offshore wind for the first time,” the report says.

The heavy inter-dependency between offshore wind and other sectors, as illustrated in Figure 5, continues to be a major capital cost issue: “The offshore wind industry has so far ridden on the back of other sectors, and so has been subject to the conditions in those markets.”

The report suggests that measures to accelerate de-coupling of the supply chain have the potential to increase competitive pressures and also to improve the likelihood that industry maturation effects (scale, learning and innovation) will feed through to project capital costs.

However, even if effective action is taken by government and industry now, the benefits are not likely to have a deflationary impact on capital costs until 4-6 years from now due to the substantial lead time required to establish new facilities. “This shift in the supply base will need a combination of market pull (long-term frame-orders and strong policies) in combination with substantial direct support for new facilities, such as grants and soft loans. If implemented successfully, these measures have the potential to re-invigorate the industry with real commercial competition driving down contract prices, pushing forward innovation and removing the ‘risk-premium’ which is currently throttling the sector,” the report says.

The very high euro content of offshore wind projects has exposed the industry to massive currency risk and since mid- 2007 the precipitous decline in the value of sterling against the euro has had a direct impact on capital costs for UK projects, of the order of 15-20%, the report estimates, noting that “increasing ‘UK produced’ content in the value chain has the potential to avoid a repeat of this in the future.”

An uncomfortable finding

The interactions between the onshore wind market and offshore supply chain against the uncertain macro economic backdrop is found to be central when considering the outlook for offshore wind capital costs. Analysis in the report “yields the uncomfortable finding that a prolonged recession and/or the cooling of the global onshore wind market results in a favourable projection of offshore wind capital costs.”