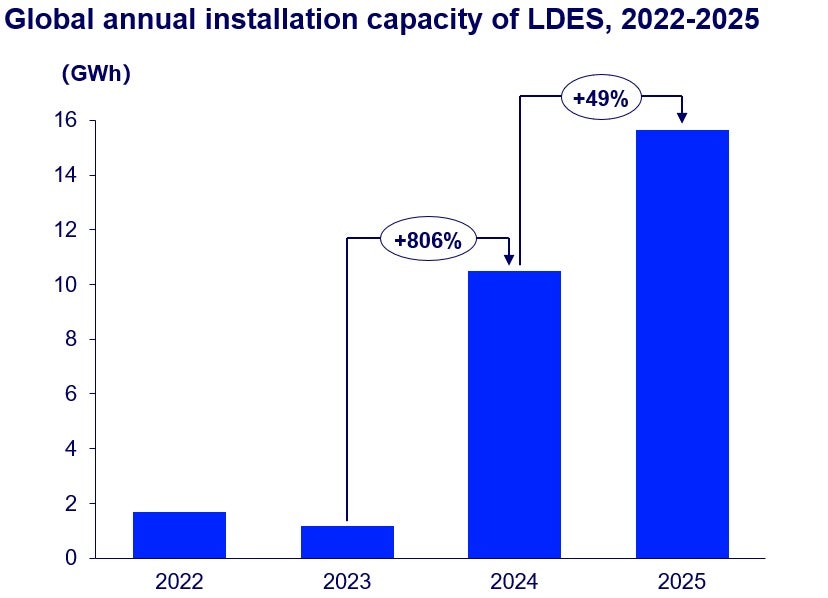

Global long-duration energy storage (LDES) installations passed 15 GWh in 2025, up 49% year on year, but Wood Mackenzie says the sector is entering a harder phase as investment slows and lithium-ion batteries extend their reach into longer-duration applications. The consultancy’s latest Long Duration Energy Storage Trends report says the market is expanding in volume but still lacks the revenue certainty needed to scale commercially in most regions.

China dominated the market, accounting for 93% of cumulative global deployment, supported by provincial mandates and the country’s Special Action Plan for Development of New Energy Storage (2025-2027). In 2025, compressed air energy storage made up 45% of installations, thermal storage 33%, and vanadium redox flow batteries 21%.

Despite that progress, Wood Mackenzie argues LDES technologies are being squeezed between rising clean-power demand and the rapid improvement in lithium-ion economics. The report says lithium-ion batteries have already captured the commercially important four- to eight-hour segment, leaving LDES to compete in markets that often do not yet pay enough for multi-hour or multi-day flexibility.

Investment conditions have also deteriorated. Global LDES funding fell 30% in 2025, excluding the US Department of Energy’s US$1.76 billion commitment to Hydrostor, while venture capital dropped 72%. High interest rates, cheaper lithium-ion pricing and competition for capital from data centres and grid infrastructure are all weighing on project pipelines.

Wood Mackenzie says the long-term opportunity remains large, but the industry will need stronger procurement frameworks, capacity mechanisms and more tailored market design if it is to move beyond demonstrations and into bankable deployment. Its net-zero scenarios suggest average storage duration must rise from 2.5 hours to about 20 hours globally, underlining why the sector still matters even if its commercial path remains difficult.