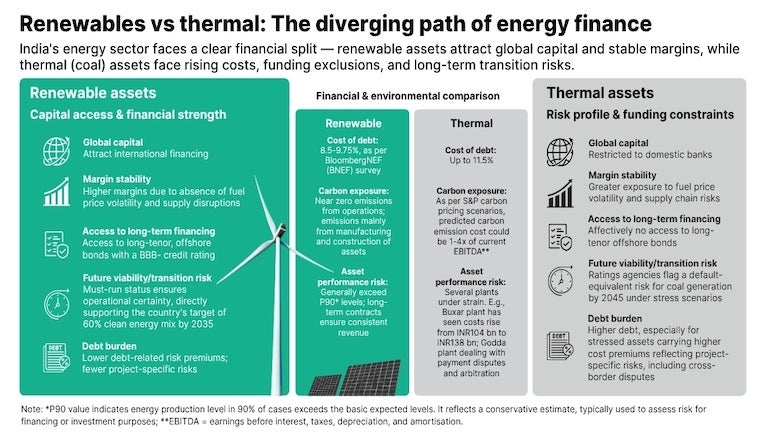

A new study by the Institute for Energy Economics and Financial Analysis, titled “Financing the energy transition: A credit perspective on India’s power sector”, finds that credit markets are already structurally differentiating between renewable and thermal assets, with renewables delivering stronger margins and better access to capital.

India is targeting 500 GW of renewables, and 60% non-fossil fuel energy in its overall mix by 2035, with financing its next big hurdle. Meeting the country’s revised Nationally Determined Contributions will depend as much on structure of debt finance as on technology or policy. Financing needs are anticipated to rise to USD 145 billion annually by 2035 for renewables, making debt markets, rather than just technology or policy, central to the energy transition. India’s dependence on imported fossil fuels, for crude oil and liquefied natural gas (LNG) for power, leaves its economy acutely exposed to geopolitical shocks and supply disruptions, reinforcing the urgent need to accelerate transition.

Key takeaways:

- Annual investments in renewables, storage and transmission are estimated to surge from USD68 billion (INR6.18 trillion) by 2032 to as much as USD145 billion (INR13.19 trillion) by 2035.

- Credit markets are already structurally differentiating between clean and thermal assets: Renewable platforms deliver stronger margins, lower variable costs, and broader access to capital than their thermal peers.

- With a sovereign-aligned credit rating and a planned capex of INR7 trillion (USD 80 billion) through to financial year 2032, NTPC Ltd, India’s largest state-owned power utility, is uniquely placed to anchor large-scale, low-cost transition financing and catalyse broader capital flows across the sector.

- India’s corporate bond market remains structurally underdeveloped, with loans the dominant funding channel across the economy. Over-reliance on more mobile international capital flows also exposes the energy transition to sudden foreign capital repatriation.

The report finds that not all players will face transition risks equally. Financially constrained players will face a dual challenge: limited balance sheet flexibility to adapt decarbonisation strategies, alongside increasingly restricted access to the funding sources that remain available to higher-quality credits. State-owned enterprises like NTPC and SJVN benefit from implicit government backing that provides refinancing flexibility unavailable to private issuers. Among the utilities, NTPC is central to unlocking transition finance. It is India’s largest integrated power utility accounting for around 17% of installed capacity, with 51.1% government ownership and a credit rating aligned with sovereign debt.