A few years ago hydrogen was the answer to decarbonisation prayers. It was seen at that time as an all-purpose tool for the energy transition and it was considered likely to have many uses in areas that were particularly difficult to decarbonise. That included as a direct replacement for natural gas in high-temperature industrial processes or power generation, as long term energy storage, in heavy transport where batteries were impractical, or even in domestic gas networks. In 2024 the US DoE Regional Clean Hydrogen Hubs Program (H2Hubs) included up to $7 billion to establish seven regional ‘clean hydrogen hubs’ across the USA, and on 20 November US Secretary of Energy Jennifer M. Granholm said it would “kickstart a new domestic hydrogen industry that can produce fuel from almost any energy resource in virtually every part of the country and that can power heavy duty vehicles, heat homes, and fertilize crops.”

Three facets of the hydrogen industry have to be commercialised to realise that vision. They are hydrogen supply, demand and transport.

Moving electrolysers down the cost curve

Almost all hydrogen production is currently from steam reforming of fossil fuels. Low-carbon production would require the addition of carbon capture and storage (CCS) to that process, or bypassing fossil fuels altogether, the use of renewables to power electrolysis to split water into its constituent hydrogen and oxygen. The latter has the support of campaigners who believe the energy transition should mean moving away from any extraction and use of fossil fuels. But it has also caught the eye of the renewable and nuclear industries as a way of turning the problem of abundance into an asset. Basing low-carbon electricity generation around wind and solar (potentially with nuclear) is expected to result in over-supply at some times (and under-supply at others). This excess could be used to power electrolysers to produce and store hydrogen from water. What is more, electrolysers share some of the characteristics – small unit size, fast development cycle and commercial-scale manufacturing of thousands of units – that have helped technologies like PV and batteries move rapidly down the cost curve.

It seems like a virtuous circle. So much so that many countries with renewable resources published plans to become major hydrogen exporters – Brazil even announced that it would develop major industries in offshore wind and in hydrogen produced by electrolysis, as a mutually supporting strategy.

The UK government has recently confirmed funding via HAR1 (First Hydrogen Allocation Round) for 11 electrolytic green hydrogen production projects totalling 125 MW: Barrow Green Hydrogen; Bradford Low Carbon Hydrogen; Cromarty Hydrogen; Green Hydrogen 3; HyBont; HyMarnhan; Langage Green Hydrogen; Tees Green Hydrogen; Trafford Green Hydrogen; West Wales Hydrogen; Whitelee Green Hydrogen. A second round, HAR2, could support some 875 MW of additional electrolyser capacity.

Transport options

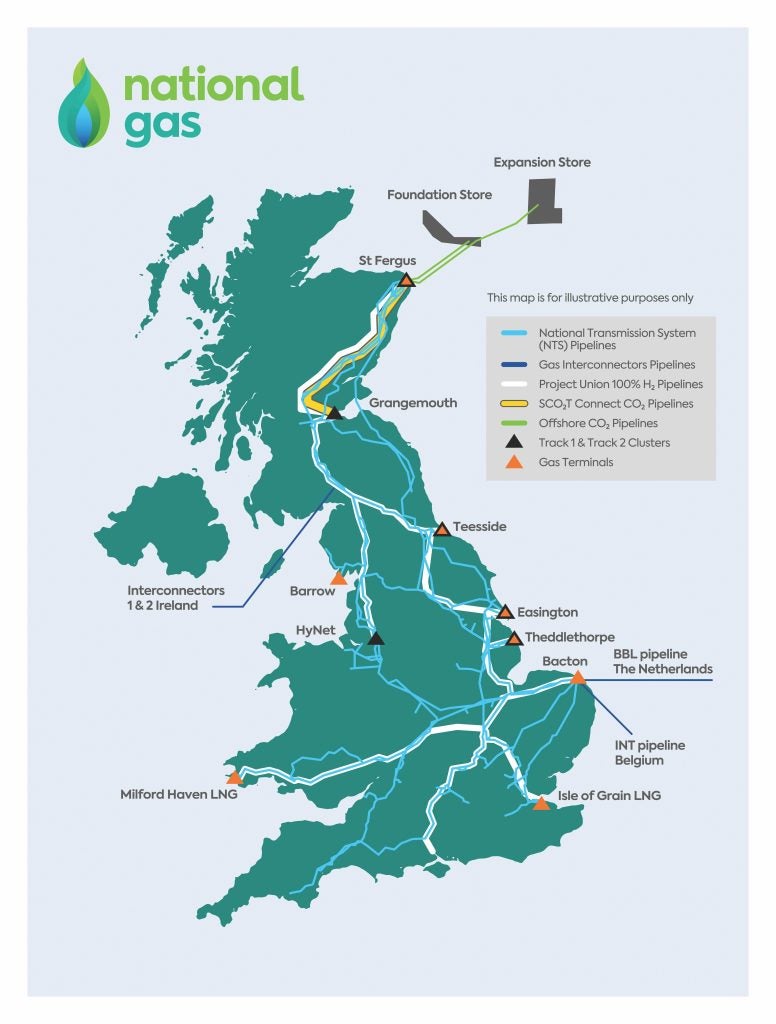

For hydrogen production plans to be realised they have to be matched by the ability to transport hydrogen to its users. This could be done using hydrogen pipelines, following the example of the fossil gas (mainly methane) industry. Hydrogen pipelines are developed technology, although IRENA (International Renewable Energy Agency) figures say there are less than 5000 km of hydrogen pipelines worldwide. In some cases, hydrogen could be transported through repurposed fossil gas infrastructure and in the UK, technical investigations have been carried out and plans announced by National Gas for ‘Project Union’ – a ‘hydrogen backbone’ using repurposed methane pipelines (see map).

In 2024 Germany’s Federal Network Agency (Bundesnetzagentur) gave the go-ahead to a 9040 km hydrogen pipeline network connecting demand clusters with hydrogen sources that will include both repurposed methane gas pipelines and new hydrogen pipelines. The high capital cost and uncertainty over the eventual users of a hydrogen network will mean that they have to be underwritten by the government.

Hydrogen pipelines would not be feasible for export-orientated hydrogen programmes such as that of Brazil. Instead, the industry will have to follow the fossil gas industry and find ways to transport hydrogen by ship. Fossil gas is transported as liquefied natural gas (LNG) and similar technology is under investigation for hydrogen. Hydrogen’s different characteristics in terms of compression and liquefaction, however, suggest the energy required and the costs of transport will be higher than for fossil gas. Other options, such as adsorbing hydrogen onto a solid material, or using an organic liquid as a transfer medium, are also at an early stage.

One transport medium that has sparked interest is ammonia, created from hydrogen at its production site and shipped in that form. There is a mature global ammonia market because of the importance of ammonia in making fertiliser (which is of course a major market for green hydrogen in any case). This might allow the hydrogen industry to use the global ammonia industry to build up its customer base, either directly – ammonia can be used as a fuel in power plants, although it produces NOx emissions that have to be managed – or splitting the hydrogen from the ammonia.

Changing use cases

None of these transport options comes without significant energy requirements at both the start and the end of the journey and the need to invest in port or terminal infrastructure.

What progress is being made on the demand side of the hydrogen triangle? Of course there are sectors that already use hydrogen (such as fertilisers and industries that require high-temperature direct heat) and that are expected to take most of the early production of low-carbon hydrogen to reduce their carbon emissions. Otherwise, the initial view of hydrogen as an all-purpose tool has changed.

Michael Liebreich from Bloomberg New Energy Finance has encapsulated the changing view of use cases for hydrogen in a ‘hydrogen ladder’, updated several times, that allocates potential hydrogen according to whether the hydrogen option is ‘unavoidable’ or ‘uncompetitive’. In the most recent (fifth) version, the most economic and necessary uses of hydrogen are not in the ‘energy’ sector at all, but in chemical processes, first in the list being fertiliser production. Global trade in ammonia and in urea for fertiliser use are both more than 180 Mt per year, and the industry is hoping to decarbonise by replacing current high-fossil hydrogen (produced by steam reforming gas, coal and oil) with its green equivalent.

In the long term, it seems likely that hydrogen will take on those aspects of power supply and security that are not easily delivered by renewables or nuclear. In a report produced in November for the UK government, the GB National Energy System Operator (NESO) set out ‘Clean Power 2030’ pathways in which it said over 80% of power would be provided by offshore wind and nuclear. It added that “After 2030, low carbon dispatchable power could be built up to replace the need for the remaining unabated gas generation.” Unabated gas plants make up less than 5% of total annual generation but NESO said the system had to be able to cope with sustained cold periods with low wind, where they “play a critical and sustained role over several hours or days.”

NESO adds, “Hydrogen in the long run can be produced via electrolysis at times of high renewable output and stored for later use when renewable output is low, without reliance on fossil gas or residual emissions”. But hydrogen storage “appears unlikely before 2030.”

That fits with Liebreich’s hydrogen ladder, which foresees hydrogen as a storage medium for use in ‘long term gas balancing’, with a secondary role in short term grid balancing (a role otherwise being increasingly fulfilled by batteries).

That general consensus is also echoed by Japan, whose Agency for Natural Resources and Energy (part of METI (Ministry of Economy, Trade and Industry) said in a recent hydrogen summary that its likely uses are in the mobility, industry and power generation sectors. It said, “By replacing fuels used at thermal power stations with hydrogen, carbon dioxide emissions can

be reduced”.

METI says Japan has a “technical advantage in hydrogen power generation”, citing Mitsubishi Heavy Industries, which is aiming to replace natural gas in turbines completely with hydrogen by “developing suitable equipment for mono-firing.”

Towards the 100% hydrogen power plant

The goal for NESO and other network operators is a power plant that can be fuelled with 100% hydrogen. In late 2024 GE Vernova said it would claim that with its LM6000VELOX package, which includes an aeroderivative gas turbine it says will operate on 100% renewable hydrogen, to be supplied to Australia.

The Australian project is also one that brings together supply of hydrogen and demand customers, without the need for transport infrastructure. The four unit power plant (200 MW in total) will power the Whyalla hydrogen site in South Australia, which will include 250 MW of electrolysis capacity for hydrogen production, using renewable energy from large wind and solar farms, and hydrogen storage. The Whyalla hydrogen power plant will also provide grid stability services.

Integrated projects like this help bring technology to maturity and increase hydrogen volumes. Putting together all the components of such a project where different parties are involved in supply, demand and transport is much more complex and requires strong legal underpinning and an allocation of risk and reward that means all parties are comfortable for the long term.

Meanwhile, in the UK, SSE and Siemens Energy have launched “Mission H2 Power” – a collaboration which also aims to deliver gas turbine technology capable of running on 100% hydrogen.

The project builds on an existing partnership between SSE and Siemens Energy and is focused on the decarbonisation of SSE’s Keadby 2 power plant, which employs a Siemens 9000HL gas turbine.

Siemens Energy plans to develop a combustion system for the HL gas turbine capable of operating on 100% hydrogen, while maintaining the flexibility to operate with natural gas and any blend of the two. This will see additional combustion testing facilities for large gas turbines constructed at Siemens Energy’s Clean Energy Centre in Berlin.

Securing investment

Securing long term investment in green hydrogen projects requires there to be offtake customers and this has been one of the factors behind cancelled projects. Gases company Air Products continues to invest in hydrogen, but in response to activist investors it stressed that it executed its green hydrogen strategy “in a prudent manner, only approving new projects after securing anchor customers and securing off-take commitments for at least 75 per cent of the output of our existing clean hydrogen projects.”

Across the nascent hydrogen industry projects have been scaled back and cancelled. That need not be a cause for dismay. New industries and technologies often go through a period of high ambition and expectation that quickly rebounds into a period of disappointment and retrenchment, before finding a stable level for the long term where demand meets supply. This is a general ‘reality check’ in hydrogen plans, for an industry whose product has changed from being considered an all-purpose tool to meeting particular needs. Hydrogen is going through this process of hype and disappointment; the result should be that its true long term role will be revealed.